Billing, payments, policy documents, and ID cards are everyday insurance service moments. When they are hard to complete digitally, customers do not see a back-office issue. They see a poor policyholder experience.

Billing is one of the highest-frequency insurance service moments

Claims often receive the most attention in insurance customer experience planning, but billing may be the interaction policyholders encounter more often. Customers want to know what they owe, when it is due, whether a payment posted, where to find receipts, how to update payment methods, and how to access policy documents or ID cards. When those tasks are difficult, they turn into calls, emails, agent requests, and avoidable service work.

Insurance billing self-service should be treated as a customer experience priority, beyond finance or back-office processing. A policyholder may not separate the billing system from the insurer’s overall digital experience. If the payment journey is confusing, the document library is hard to find, or policy access requires too many steps, the customer experiences the brand as difficult to work with.

Recent insurance digital experience research has highlighted policyholder demand for streamlined billing, payments, and document access. That demand is practical. Most customers are not looking for a flashy insurance app. They are trying to finish routine tasks quickly and with confidence.

The billing questions that create avoidable contact volume

Billing-related service volume often comes from simple questions that digital channels should answer clearly: Did my payment go through? Can I see my payment history? Where is my renewal document? Can I download my ID card? What payment method is on file? Why did the premium change? What happens if I miss the due date?

The issue is not always that the insurer lacks a portal. The issue is that the billing journey is not designed around the customer’s question. A payment button alone does not answer whether a transaction posted. A document tab alone does not help if policyholders do not know which document they need. A billing page alone does not reduce calls if it lacks confirmation, history, next steps, or clear contact paths for exceptions.

What strong insurance billing self-service should include

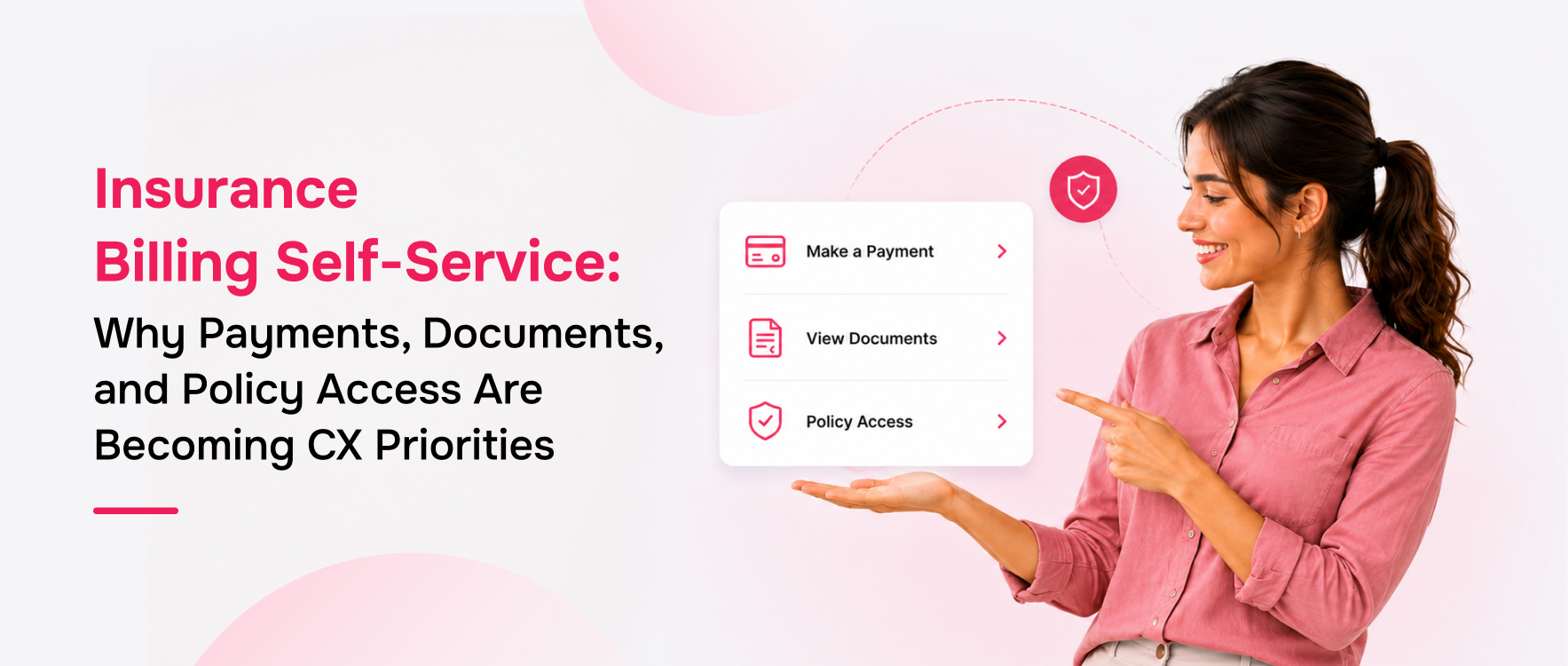

A useful insurance billing self-service experience should include secure account access, clear premium due information, payment status, payment history, digital receipts, policy documents, ID cards, renewal documents, and easy navigation to support. Depending on the insurer’s systems and payment rules, it may also include saved payment methods, autopay management, installment schedules, notifications, and document delivery preferences.

The important point is that these features should work together. A policyholder who receives a payment reminder should be able to open the mobile app or portal, see the amount due, pay or confirm payment, access the receipt, and understand the next step. A small-business customer managing multiple policies should be able to locate documents and payment information without switching between disconnected pages.

Why billing self-service affects retention and trust

Billing is a trust moment because money, coverage, and continuity are connected. If customers are unsure whether they paid, whether coverage remains active, or whether documents are current, anxiety increases. Clear digital billing journeys help reduce that uncertainty.

This does not mean billing self-service replaces agents or service teams. It means routine tasks should not require human support unless there is an exception. When digital billing works well, service teams can spend more time on complex billing questions, coverage concerns, disputes, and customers who need personal help.

Where Xemplar Engage comes into play

Xemplar Engage gives insurers and MGAs a practical way to bring billing-adjacent service moments into the policyholder’s digital experience. Its insured portal and branded mobile app can support access to policy information, documents, ID cards, claims, notifications, and account-level service workflows. The value is not simply giving policyholders another login. The value is helping them complete routine tasks in a branded, connected environment.

For insurers with legacy systems, this engagement-layer approach matters. Many organizations cannot replace billing, policy administration, claims, and document systems all at once. A configurable self-service layer can help policyholders interact with the information and workflows they need while insurers continue to modernize the underlying systems.

How insurers can prioritize billing self-service improvements

The fastest way to prioritize billing self-service is to review the questions that already reach the contact center, agents, and service inboxes. If customers repeatedly ask for payment confirmation, start with payment status and receipts. If they ask for ID cards or policy documents, improve document access and navigation. If they call after every reminder, review reminder wording, timing, and the landing page experience.

This keeps the roadmap grounded in actual demand. Billing self-service should not be built around a wish list of features. It should be built around the tasks policyholders are already trying to complete and the service volume insurers are already absorbing manually.

Insurers should also segment billing needs by customer type. A personal lines customer may need quick payment and ID card access. A small business may need documents, multiple contacts, payment records, renewal materials, and proof of coverage. An MGA may need to support policyholders while coordinating with carrier or payment partners. These differences should shape the workflow.

Implementation checklist for insurance billing self-service

A practical billing self-service rollout should begin with the top five billing contact drivers, then map each driver to a digital action. Payment confirmation should connect to receipt access. Due date confusion should connect to clearer billing summaries. Document requests should connect to searchable policy and billing documents. Renewal questions should connect to renewal notices and support paths.

The experience should also include content ownership. Billing language can change when products, fees, payment rules, or regulatory requirements change. A strong digital journey needs a named owner who can keep payment explanations, document labels, and reminder messages current.

Finally, insurers should test the journey from the policyholder’s view. Can a customer complete the task on mobile? Can they understand the confirmation? Can they recover if payment fails? Can they find help without starting over? These details determine whether self-service actually reduces service volume.

FAQs

- What is insurance billing self-service?

Insurance billing self-service lets policyholders view billing information, make or confirm payments, access receipts, download policy documents, and manage routine payment-related tasks digitally. - Why does billing self-service matter for insurers?

It reduces avoidable service calls, improves payment confidence, gives customers faster access to documents, and strengthens the overall policyholder experience. - What should an insurance payment portal include?

A useful portal should include amount due, due dates, payment status, payment history, receipts, policy documents, ID cards, renewal documents, and support paths for exceptions. - How does Xemplar Engage support billing self-service?

Xemplar Engage supports branded mobile and portal experiences that can connect policyholders to policy, document, notification, billing-adjacent, and support workflows.