MGAs need modern digital service, but they often do not have carrier-size IT teams or fully unified back-end systems. That makes the engagement layer especially important.

MGAs face a different digital experience challenge

MGAs, program administrators, and specialty insurance teams often compete on speed, niche expertise, and service quality. But their digital infrastructure may depend on multiple carrier, TPA, billing, claims, document, and policy systems. That creates a practical challenge: policyholders expect modern self-service, while the MGA may not have the budget or internal IT capacity of a large carrier.

This is why digital experience for MGAs should not be framed as a generic modernization story. The issue is operational specificity. MGAs need to give customers, agents, and internal teams better access to service workflows without taking on a multi-year core-system replacement project.

What policyholders expect from MGA digital service

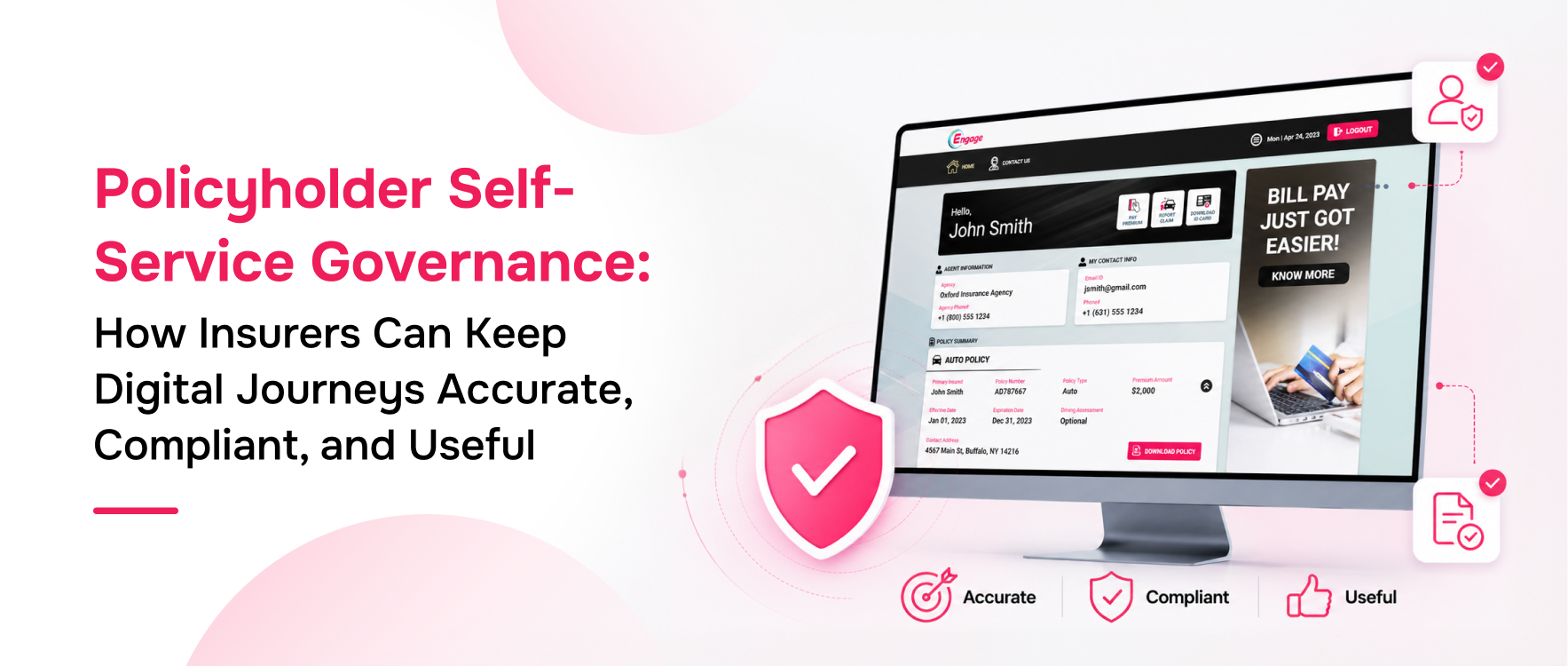

Policyholders rarely think about the operational structure behind their policy. They want to access documents, download ID cards, check billing information, receive alerts, submit information, review claim updates where available, and ask for support without navigating a maze of disconnected systems. If the experience is fragmented, the MGA or program brand may receive the blame even when the underlying system belongs to another party.

For commercial or specialty programs, the need can be even more complex. A small business may manage multiple vehicles, locations, certificates, documents, users, or coverages. A household may have multiple policies. A producer may need quick answers for a client. The digital layer has to make account and policy access easier, not simply place a login in front of a complex back end.

Why carrier-grade does not have to mean carrier-size IT

Carrier-grade digital experience means reliable, branded, secure, and useful service journeys. It does not necessarily mean the MGA must build a custom platform from the ground up. A configurable engagement layer can help MGAs expose the right workflows to policyholders while connecting to existing processes and systems where appropriate.

This approach is valuable because it matches how many MGAs actually operate. They may need fast deployment, branded experiences, workflow configuration, notifications, portal access, mobile access, and administrative visibility. They may not need or want a massive internal engineering program before improving customer service.

The MGA workflows that benefit most from self-service

The strongest starting points are high-frequency service moments: policy document access, ID cards, payment or billing access where enabled, renewal communication, claim-related information, document submission, contact updates, notifications, and support routing. These workflows create avoidable calls when they are not easy to complete digitally.

MGAs should prioritize workflows based on service volume and customer confusion. If agents or service teams repeatedly answer the same document questions, start there. If policyholders call after every renewal communication, improve renewal document access and notification clarity. If claim-related confusion drives inbound volume, create clearer claim communication and documentation paths.

Where Xemplar Engage comes into play

Xemplar Engage is a strong fit for MGA digital experience because it supports branded policyholder engagement through mobile, portal, chatbot, notification, and admin capabilities. The relevant message is that MGAs can offer a modern self-service experience without positioning themselves as a technology company or hiring a carrier-size IT organization.

For Xemplar Engage, this article should speak directly to MGA operating constraints: lean teams, multiple partners, fragmented systems, program-specific workflows, and the need for branded service. The product should appear as the practical way to create a connected engagement layer around existing insurance operations.

How MGAs should evaluate digital experience success

MGAs should measure success through operational and customer indicators. Useful benchmarks include reduction in document-related service requests, mobile or portal adoption by policyholders, completion of common self-service tasks, claim or billing inquiry reduction, notification engagement, support routing accuracy, and internal administrative time saved.

This gives digital investment a business case. Instead of saying the MGA needs a portal because competitors have one, the argument becomes clearer: better digital access reduces avoidable contact, improves policyholder confidence, supports agents, and helps lean teams deliver a more consistent service experience.

What MGAs should ask before selecting digital experience technology

MGAs should evaluate technology based on workflow fit, speed of configuration, branding control, integration approach, administrative visibility, policyholder usability, and support for future growth. The question is not whether a platform has every possible insurance feature. The question is whether it can help the MGA improve the service journeys that create the most policyholder and agent friction today.

Important evaluation questions include: Can policyholders access documents easily? Can the experience reflect the MGA’s brand? Can workflows be configured by program or product line? Can notifications support service needs? Can the tool work around fragmented insurance systems? Can internal teams see enough engagement data to improve operations?

This buyer lens makes the topic commercially useful. It speaks to MGA leaders who need practical modernization, not abstract digital modernization.

Implementation checklist for MGA digital experience planning

MGAs should begin with a service-volume audit. Which requests consume the most time for internal teams, agents, or carrier partners? Common candidates include document requests, ID cards, billing questions, claim updates, certificate requests, and renewal communication. These are usually better starting points than broad modernization initiatives.

Next, MGAs should define which workflows must be branded and controlled by the MGA and which can remain connected to carrier or partner systems. This distinction helps avoid overbuilding. The goal is to give policyholders a clearer experience even when the back-end ecosystem remains complex.

Finally, MGAs should choose metrics that match lean-team realities: fewer repetitive calls, faster document access, higher self-service completion, better notification engagement, and improved visibility for administrators.

How this supports agent and partner relationships

MGA digital experience also affects producers and partner teams. When policyholders cannot access documents or understand basic service steps, agents often become the workaround. Better self-service reduces that burden and helps agents focus on advisory work, renewals, coverage questions, and relationship management. A branded engagement layer can also help MGAs present a more consistent experience across programs, even when underlying carrier or partner systems differ.

FAQs

- What is digital experience for MGAs?

Digital experience for MGAs refers to the mobile, portal, notification, document, billing, claim, and support workflows that help policyholders and agents interact with an MGA digitally. - Why do MGAs need self-service portals?

MGAs need self-service portals to reduce repetitive service requests, improve document access, support policyholder convenience, and offer a more carrier-grade experience. - Can MGAs improve digital service without replacing core systems?

Yes. A configurable engagement layer can improve customer-facing workflows while connecting to existing systems and processes where appropriate. - How does Xemplar Engage help MGAs?

Xemplar Engage helps MGAs create branded mobile and portal experiences with digital service workflows, notifications, chatbot support, and administrative visibility.