Most insurers can take a claim online. That does not mean they have fixed the claims experience.

The real test starts after first notice of loss. Can the policyholder see what is happening? Can they upload the right evidence without calling? Can the insurer collect clean information, reduce adjuster rework, and keep the customer informed without forcing channel switching?

That is where many digital claims programs still break.

For U.S. insurers and MGAs, this is not only a customer experience issue. It is a claims operating issue. Every missing photo, unclear damage description, repeated status call, and unresolved handoff creates expense. The policyholder feels it as frustration. The carrier sees it as adjuster drag, longer cycle time, avoidable contact volume, weaker digital adoption, and higher retention risk.

The data is already pointing in that direction. J.D. Power found that receiving adequate digital updates is one of the top drivers of claims digital satisfaction, but insurers deliver those updates only 22% of the time. The same study found that only 36% of auto insurance customers and 31% of homeowners insurance customers receive claim status updates through mobile apps. Insurity also found that 22% of consumers have avoided filing a claim because the process was too frustrating or complicated, while 64% would consider switching insurers for a better digital experience.

The conclusion is uncomfortable but useful: digital claims tools exist, but the claims journey is still not connected enough.

The real gap is claims journey continuity

A portal can accept a claim. A mobile app can collect photos. A chatbot can answer basic questions. None of that matters enough if the tools do not share context with the actual claims workflow.

Policyholders do not experience a mobile app, a web portal, a chatbot, an email notification, and a claims representative as separate channels. They experience one claim. When those channels are not aligned, the customer becomes the integration layer.

That is the maturity step insurers need to prioritize in 2026. The goal is not to add another digital surface. The goal is to connect the journey from FNOL through evidence capture, status updates, escalation, and resolution.

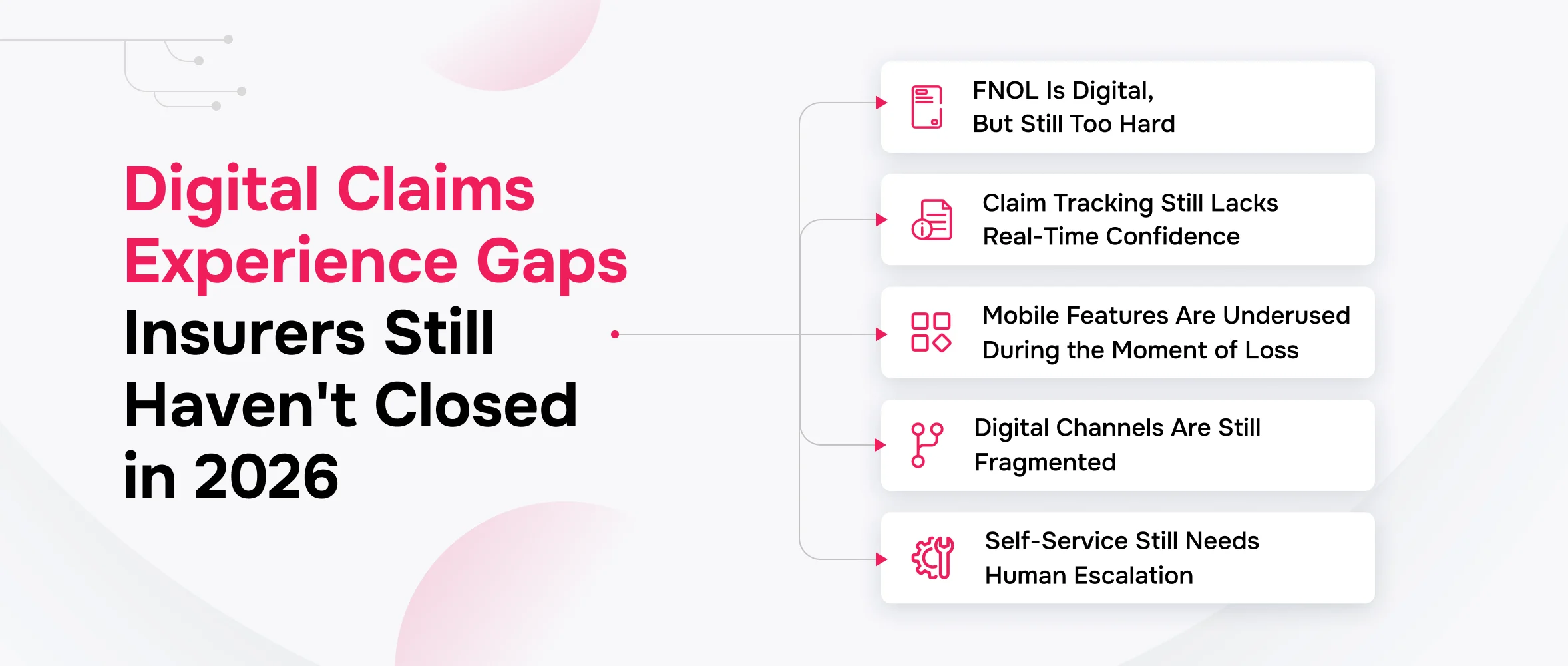

Gap 1: FNOL is digital, but still too operationally fragile

First notice of loss should be fast, guided, and clear. Too often, it still feels like an internal claims script converted into a web form.

That is not good enough for the policyholder, and it is not good enough for claims operations. A weak FNOL experience creates incomplete submissions, missing media, vague descriptions, avoidable callbacks, and slower assignment. The customer thinks the claim has started. The adjuster receives a file that still needs cleanup.

A stronger digital FNOL experience should guide the claimant through the right questions, validate inputs in real time, collect photos or videos, capture incident details while they are fresh, and explain what happens next. The operational value is simple: cleaner intake, less rework, faster triage, and better adjuster capacity.

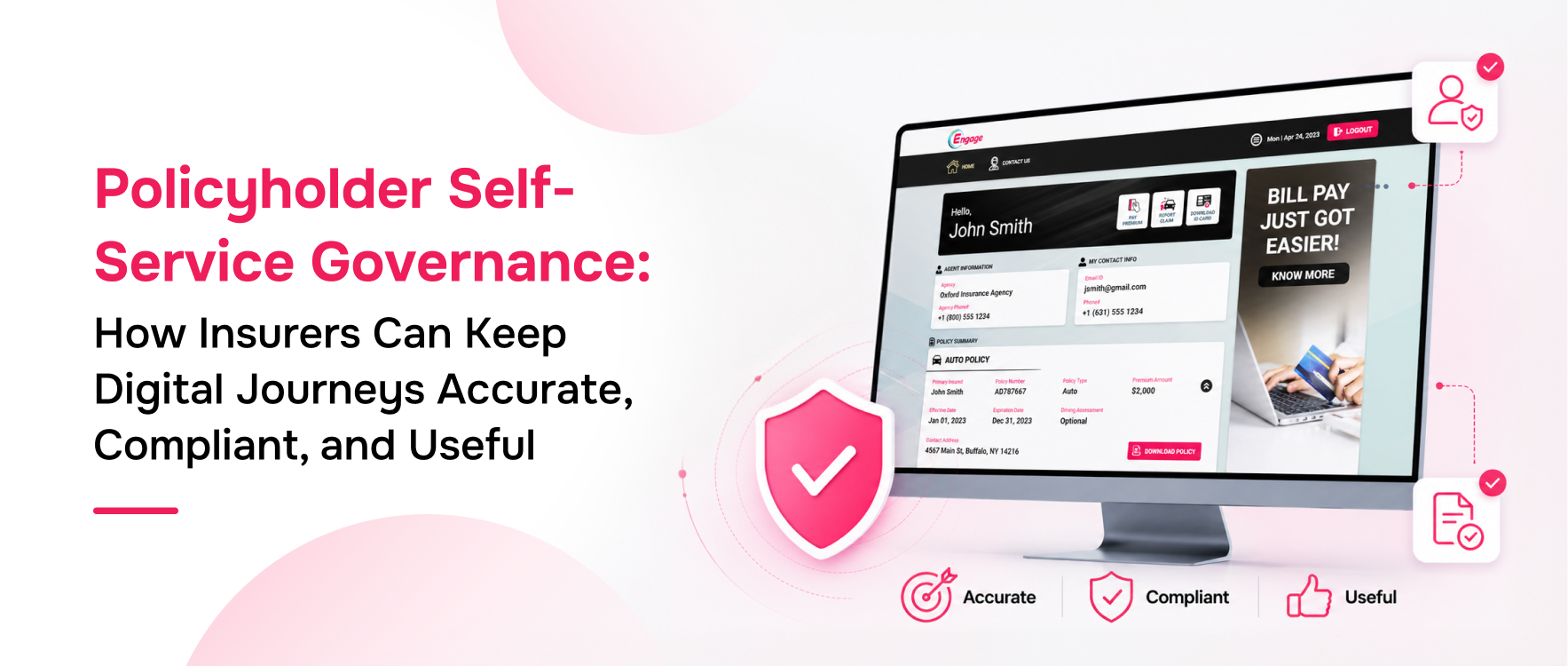

Xemplar Engage fits this problem because it supports mobile and web-based claim initiation, media uploads, and self-service workflows that help insurers collect better claim information earlier in the journey.

Gap 2: Claim tracking still does not answer the customer’s real question

Policyholders do not only want to file claims online. They want to know what is happening after submission.

A status label like in review is not enough. It does not explain what was received, what is missing, who is reviewing the file, what happens next, or when the customer should expect another update.

This is where trust erodes. Customers do not call because they love calling. They call because the digital experience has not answered the question that matters.

For insurers, weak claim tracking shows up as avoidable inbound volume, callback pressure, frustrated adjusters, and lower confidence in digital self-service. J.D. Power also found that 22% of customers still rely on multiple channels to find answers to the same question. That is not multichannel success. That is digital uncertainty.

Better claim tracking should use plain language, proactive notifications, milestone visibility, and clear next steps. The policyholder should not have to decode the claims workflow.

Gap 3: Mobile is underused when evidence is fresh

A mobile app should do more than display policy documents. During a claim, it can help capture the right information at the right time.

The moment of loss is time-sensitive. Photos, location, incident details, witness information, damage descriptions, weather context, and supporting documents are often easiest to collect immediately. If the mobile experience does not guide that process, the insurer may lose valuable context before the claim reaches an adjuster.

Xemplar Engage highlights mobile-first claim capabilities such as claim initiation, photo and video upload, real-time claim progress tracking, roadside assistance requests, weather alerts, storm tracker updates, and hurricane preparedness tools. That matters for U.S. insurers because claims demand can spike fast, especially during severe weather events.

The better question for carriers is not whether they have a mobile app. The question is whether that app reduces loss-time friction and improves the quality of information entering the claims process.

Gap 4: The claimant sees one claim. The insurer sees six systems

Many insurers offer a mobile app, portal, chatbot, email updates, SMS, and phone support. The problem is not channel availability. The problem is context continuity.

If the chatbot, mobile app, portal, email notification, and claims representative do not share the same view of the claim, the customer has to repeat information. That turns digital into another source of friction.

Enterprise buyers should treat this as a workflow design issue. The claim journey needs consistent status information, connected document and media capture, clear handoffs, and integration with the systems where claims work actually happens.

This is where Xemplar Engage should be positioned as more than a front-end experience layer. Its value is strongest when mobile apps, web portals, AI chatbots, notifications, and back-end integrations support the same policyholder journey instead of creating disconnected digital islands.

Gap 5: Self-service still needs intelligent human escalation

Digital claims should not mean forcing every claimant into self-service. Some claims are complex, emotional, urgent, or high severity. The goal is to route routine work digitally while making human support easier to reach when the claim needs it.

The best claims experience gives policyholders control without making them feel abandoned. That means clear escalation options, intelligent routing, and proactive communication before the customer feels the need to call.

Human oversight is not a checkbox. It is a design decision. Some claims need review before action. Some need review after action. Some need exception-only review. Getting this wrong either kills efficiency or creates risk.

The goal is not fewer humans. The goal is better placement of humans.

Gap 6: Claims leaders still lack enough visibility into digital adoption

Enterprise claims leaders need more than customer-facing features. They need visibility into whether those features are being used, where claimants drop off, which channels create repeat contact, and which steps create avoidable operational drag.

Digital claims programs fail when adoption is assumed instead of measured. A carrier may have a portal, app, chatbot, and notification system, but still lack a clear view of behavior across the journey.

The stronger operating model tracks adoption, claim submission quality, upload completion, status-check behavior, escalation triggers, abandonment, call deflection, cycle time, and resolution quality. Without those metrics, digital transformation becomes a feature inventory instead of a performance system.

Xemplar Engage addresses this through an Admin Portal designed to monitor engagement, adoption, usage metrics, notifications, and performance trends. That visibility matters because insurance executives cannot improve a claims journey they cannot see.

What insurers should prioritize in 2026

Insurers do not need another disconnected claims feature. They need a claims experience that reduces effort from FNOL to resolution and gives the business measurable operating value.

- Map the real claims journey across app, portal, chatbot, SMS, email, call center, and claims systems.

- Fix FNOL completeness with guided questions, validation, and mobile media capture.

- Make claim tracking useful with plain-language status, blockers, next steps, and expected timing.

- Connect digital channels so policyholders do not repeat information or chase conflicting updates.

- Design escalation paths for complex, urgent, emotional, or high-severity claims.

- Track adoption and operational performance, including self-service usage, call deflection, cycle time, upload completion, escalation rate, and rework.

- Tie digital claims investment to claims economics, not only customer satisfaction.

Where Xemplar Engage fits

Xemplar Engage is strongest when positioned as a digital policyholder engagement platform for insurers and MGAs, not as another standalone claims tool.

The platform supports insurer-branded mobile apps and web portals, claims initiation, photo and video uploads, claim status tracking, policy services, payments, notifications, AI chatbot capabilities, and integration with back-end systems. For claims leaders, that combination matters because the experience gap is rarely solved by one feature.

The practical value is journey continuity: helping policyholders act digitally while helping insurers reduce avoidable contact, improve data quality, protect adjuster time, and monitor engagement from one operating view.

Final thought

Claims are not just a service workflow. Claims are the product being tested.

Policyholders want to file claims quickly, understand what is happening, receive updates without chasing the insurer, and move between digital and human support without starting over.

Insurers that close those gaps will not just modernize claims. They will reduce avoidable calls, improve intake quality, protect adjuster capacity, shorten cycle friction, and create a policyholder experience that feels clear when customers need clarity most.

FAQs

- What is the biggest digital claims experience gap in 2026?

The biggest gap is claims journey continuity. Many insurers allow digital claim submission, but policyholders still lack clear updates, connected channels, and plain-language next steps after FNOL.

- Why does digital FNOL matter for insurers?

Digital FNOL helps collect cleaner information earlier, reduce intake calls, minimize adjuster rework, improve triage, and shorten the time between claim submission and action. - Do policyholders prefer digital claims or human support?

They prefer convenience and clarity. Routine claims should be easy to manage digitally, while complex, emotional, urgent, or high-severity claims should offer fast human escalation. - How can insurers reduce claims call volume without hurting the customer experience?

Insurers can reduce avoidable claims calls by improving FNOL guidance, sending useful claim status updates, connecting app and portal workflows, and giving policyholders clear next steps before they feel the need to call. - What should insurers measure when improving the digital claims experience?

Insurers should track self-service adoption, FNOL completion quality, upload completion, claim status engagement, call deflection, escalation rate, cycle time, rework, complaint trends, and retention after claim. - How does Xemplar Engage support digital claims experiences?

Xemplar Engage supports insurers and MGAs with mobile apps, insured portals, AI chatbots, claims initiation, photo and video uploads, claim status tracking, notifications, policy services, payments, back-end integration, and admin visibility into engagement trends.