Let’s be blunt. While insurers have been perfecting risk models, a more immediate threat has been quietly eroding balance sheets: a deteriorating customer experience.

Customers no longer compare insurers to other insurers. They compare us to the seamless digital interactions they have with leading technology companies and financial institutions. They manage their lives in real time on their smartphones, yet when they need to file a claim or update a policy, they are often met with frustrating, outdated processes. This gap is no longer a minor inconvenience. It is a direct hit to profitability and enterprise value.

A recent McKinsey study confirms what many customer satisfaction scores already reveal: nearly 60 percent of policyholders describe their insurer’s digital experience as outdated or inconsistent. In an era of tight margins and rising acquisition costs, that perception is a tangible liability.

The Core Problem: Legacy Systems, Modern Expectations

The boardroom understands the urgency of digital transformation in other industries. The question is, why has insurance lagged? The reasons are operational and deeply rooted.

Technical Debt as an Anchor: Legacy policy administration systems, while stable, were never built for the seamless, API-driven world we now operate in. The cost and complexity of modernization have stalled many initiatives.

Data Silos Create Broken Journeys: Claim data sits in one system, policy data in another, and billing in a third. This fragmentation forces customers to repeat their story, breaking trust at every touchpoint.

The “Check the Box” Mobile App: Many first-generation apps were created defensively and offer little more than a digital document viewer. Adoption rates below 20 percent prove that this is not a digital strategy but a digital façade.

The result is more than customer frustration. It increases operational costs, limits cross-sell opportunities, and creates a retention risk no insurer can afford to ignore.

The Strategic Shift: From Service Center to Self-Service

The solution is not to incrementally improve call centers. The winning strategy is to empower customers through integrated, intelligent self-service platforms. This is where insurers move from defense to offense.

At our company, we have seen that platforms like Xemplar Engage are not just IT projects. They are strategic revenue engines that deliver measurable impact.

- Automate to Elevate

Up to 40 percent of call centre volume comes from simple, repetitive requests such as “I need an ID card” or “What is my claim status?” By automating these through branded web and mobile portals, insurers can reduce operational costs and free their best agents to handle high-value interactions requiring empathy and expertise. Many carriers have seen a 28 percent reduction in call volume for specific inquiry types. - Turn Claims into a Loyalty Moment

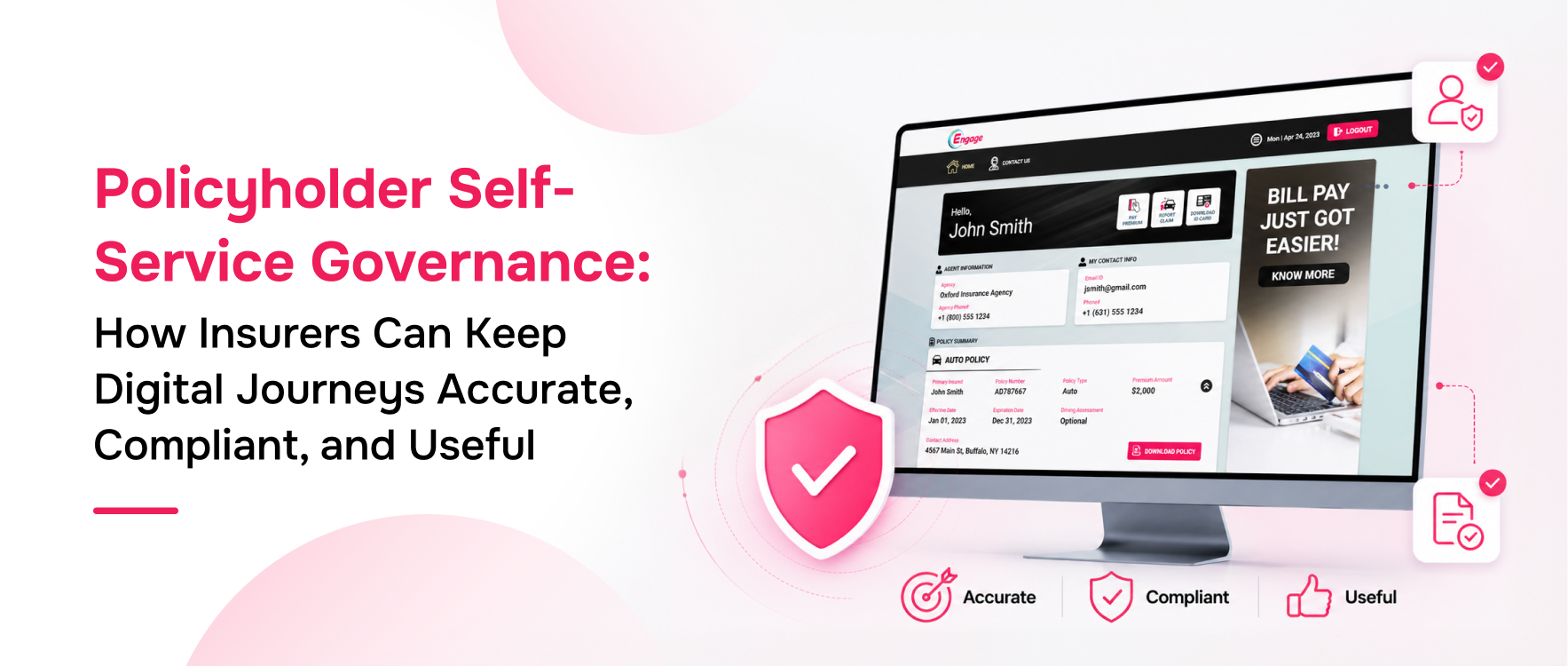

The claims process is the most critical brand touchpoint. A slow or opaque process creates detractors. A modern digital platform allows customers to submit claims via mobile, upload photos and videos, and track progress in real time. Combined with AI-driven triage and digital payments, cycle times can drop from weeks to days. This efficiency directly improves Net Promoter Scores and customer retention. - Build a Connected Ecosystem

The goal is not to build another app but to create a connected ecosystem. Xemplar Engage integrates through a robust API layer with policy, billing, and claims systems. This single source of truth simplifies compliance, eliminates silos, and delivers on the promise of a 360-degree customer view.

The Bottom-Line Impact

For the Enterprise

- Cost Reduction: Direct decrease in call center and document processing costs.

- Retention Lift: Engaged digital customers renew at rates up to 50 percent higher.

- New Revenue: Personalized in-app cross-selling at key life events such as adding a teen driver.

- Faster Time to Market: Configurable platforms allow new products and features to launch in weeks instead of quarters.

For the Policyholder

- Control: 24/7 access to policies, documents, and real-time claim status.

- Convenience: Instant ID cards, proactive renewal reminders, and digital payment options.

- Confidence: Transparent, seamless experiences that build trust when it matters most.

The message is clear. Digital self-service does not just improve satisfaction. It drives measurable business outcomes.

A C-Level Roadmap for Digital Transformation

Digital transformation succeeds only when led from the top. It requires alignment, accountability, and a shared vision.

- Audit the Friction: Quantify the true cost of current pain points. Measure call types, claims leaks, and processing delays to build a data-backed business case.

- Pressure-Test Your Tech Strategy: Evaluate technology partners by their integration capability and deployment speed. Choose partners who can demonstrate live integrations, not just presentations.

- Align the C-Suite: Marketing owns brand experience, Claims owns process efficiency, IT owns architecture, and Finance owns ROI. The CEO must align them all toward a single North Star metric.

- Launch, Learn, and Iterate: Start with a minimum lovable product, measure engagement continuously, and use behavioral data to guide development priorities.

The future of insurance belongs to those who deliver certainty and simplicity in an uncertain world. The gap between customer expectations and current service delivery is not just a problem. It is the greatest opportunity for growth and differentiation in the decade ahead.

By empowering customers with a truly modern self-service experience, insurers do more than reduce costs. They build the trust and loyalty that define long-term relevance. The time for incremental change has passed. The mandate for strategic transformation is now